2.4. Historical evolution and current situation

2.4.1. The current international situation

In 2013, Gill Seyfang and Noel Longhurst conducted a study which measured and evaluated the situation of complementary currencies on an international basis. This is one of only a few studies whose global perspective has made it possible to generate homogenized results. Despite the fact that the data shown is for 2013, the study’s comparative analysis produces a relative overview of the complementary currencies phenomenon internationally.

For the purposes of the study, the authors sought to identify complementary currency groups with at least five active projects within one country in 2013. Emergent initiatives with fewer than five active projects were therefore not included in the analysis, and nor were business exchange systems (complementary currencies of a purely capitalistic nature) or loyalty programmes based on incentives for the purchase of sustainable goods and services or recycling.

According to these constraints, a total of 38 nationally-based currency groups were found to exist in 23 countries, across six continents, representing a total of 3,418 local projects or initiatives. The term currency group refers to a group of at least five active projects, of the same type, in the same country in 2013. Each initiative is catalogued as one of the four complementary currency typologies previously presented in this COURSE: mutual exchange systems, service credit banks, local currencies and barter markets.

The most common complementary currency typology is the service credits type, with 1,715 projects (50.2% of the total) across eleven countries and four continents, followed by the mutual credit systems, with 4,412 projects (41.3% of the total) across fourteen countries and five continents. Local currency systems are the third group of complementary currencies, consisting of 243 projects (7.1% of the total) in six different countries and four continents. The last group is formed by the barter markets, representing 48 projects (1.4% of the total) across four countries and two continents.

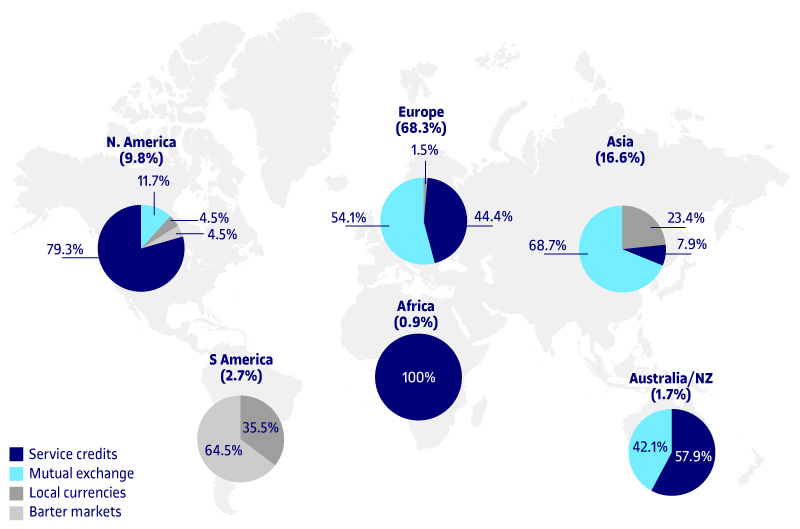

Europe has the greatest number of projects, with 2,333 initiatives (68.3%). Over half of these (54.1%) are mutual exchange systems, 44.4% are service credit banks and just 1.5% are local currencies. Asia follows, with 16.6% of the complementary currency projects. More than two-thirds of these (68.7%) are service credit banks, 23.4% are local currencies, and the rest are mutual exchange systems. North America is the third most populated region in terms of complementary currencies, with 9.8% of projects worldwide, of which the majority (79.3%) are service credit banks, mostly in the USA. South America represents 2.7% of the world’s complementary currency projects, dedicated exclusively to local currencies (64.5%) and barter markets (35.5%). Australia and New Zealand account for only 1.7% of the world’s initiatives, 57.9% of which is represented by mutual exchange systems and 42.1% by service credit banks. Finally, the countries of Africa use only mutual exchange systems, which account for 0.9% of the international total.